Accenture: Selling the Tool That Could Replace You

After a 59% collapse, is artificial intelligence still the structural threat the market now fears — or has the threat already been paid for?

01 — The Analytical Question

The paradox arrives, priced in

Accenture is the largest implementer of enterprise technology in the world, and the technology now reshaping every enterprise is artificial intelligence. The paradox sits at the center of the company: the same force driving record AI-transformation demand today is the force that could, over time, compress the labor-based model that produces Accenture’s revenue. Accenture bills for human hours at a margin over cost. Generative AI exists to reduce the human hours required to reach a given outcome. The company is, quite literally, paid to install the tool capable of shrinking its own addressable pool of billable work.

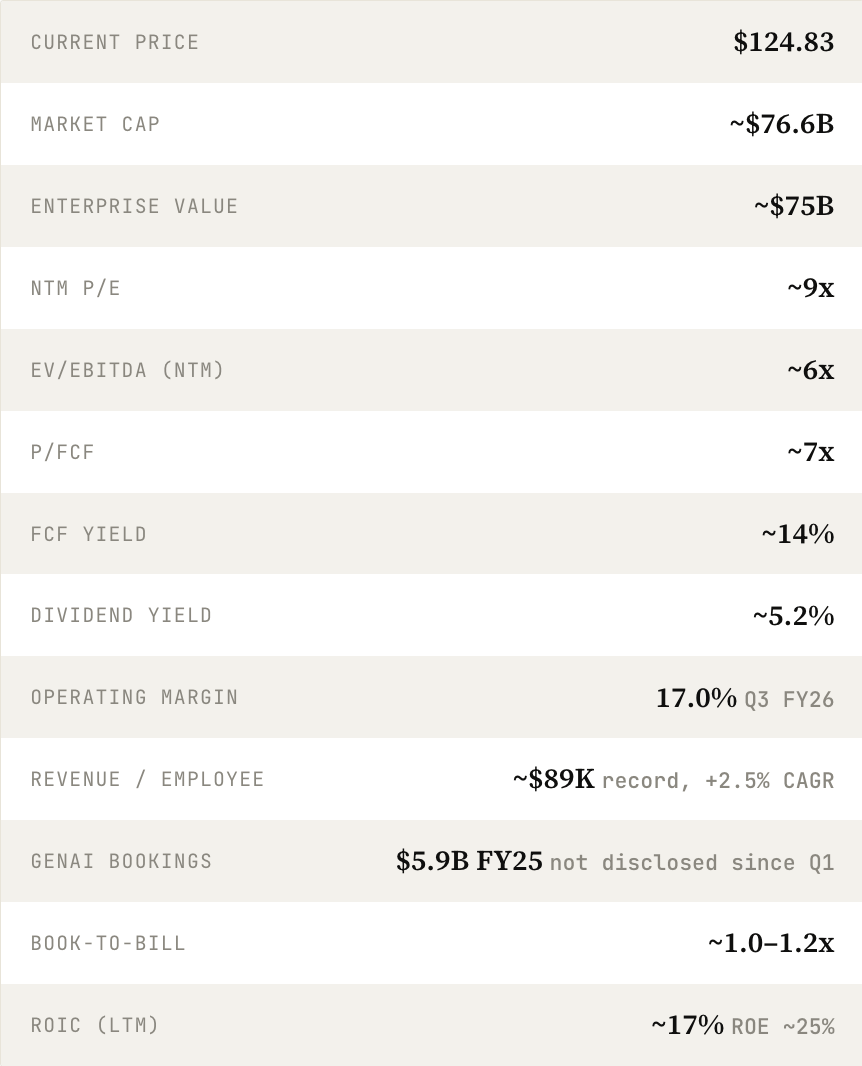

For most of the last decade that tension was abstract. It is no longer. On June 18, 2026, Accenture reported a fiscal third quarter that beat on earnings and expanded margins, then watched its stock fall roughly 18% in a single session — its worst day on record. At approximately $124.83, the shares sit at a fresh 52-week low, down about 59% from the $307.77 high set inside the past year. The multiple has collapsed with it: a trailing P/E near 10x and a forward multiple around 9x, against a five-year average closer to 28x. On free cash flow the stock changes hands at roughly 7x, a ~14% free-cash-flow yield and a ~5.2% dividend yield. This is no longer a market pricing Accenture as a serene compounder. It is a market pricing in damage.

That single fact reframes the debate. The bear case is no longer a contrarian whisper against a 28x multiple; large parts of it are now the consensus embedded in a 9x one. The argument that follows runs along three reinforcing threads — AI compressing the labor-arbitrage model, macro pressure on discretionary spend, and pricing pressure on margins — and then asks the only question that still carries an edge: how much of that combined structural threat is already paid for, and is the deterioration in the business a deceleration the franchise survives or a decline it does not? The verdict is genuinely open, and it follows the evidence rather than the lean.

02 — Business Snapshot

What the franchise actually is

Accenture sells professional services to the world’s largest organizations: strategy and consulting, technology implementation, and the ongoing operation of business processes. It works with roughly 9,000 clients, including three-quarters of the Fortune Global 100, and at quarter-end employed approximately 799,000 people — the largest professional-services workforce on earth. Fiscal 2025 revenue was $69.67 billion, up 7%, and the company is the clear number-one in IT services by revenue.

Two engines drive that revenue, and the distinction is central to the debate. Consulting (about half of revenue) is project-based: transformation programs, system implementations, advisory work. It is higher-margin, faster-recognizing, and more discretionary — the line item a chief financial officer can defer when budgets tighten. Managed Services (the other half) is the recurring engine: Accenture runs finance, procurement, supply-chain, security, and increasingly AI operations on a multi-year contractual basis. It is stickier, more defensive, and more annuity-like. The mix matters because the AI threat and the macro threat both bear hardest on the discretionary consulting half.

The economics underneath are a labor-arbitrage model. Accenture recruits, trains, and deploys consultants — a large share of them in lower-cost global delivery centers in India, the Philippines, and similar locations — and bills clients for their time at a rate above fully loaded cost. Profit is the spread between bill rate and delivery cost, multiplied by utilization. The model is capital-light to an extreme degree: property and equipment additions run around $0.7 billion against nearly $70 billion of revenue, so almost every dollar of operating income converts toward cash. The genuine “investment” line is not capital expenditure but acquisitions, of which Accenture completes dozens per year.

The moat is scale, trust, and relationship depth. Enterprises do not hand a mission-critical, multi-year transformation to an unproven vendor, and Accenture’s breadth — strategy plus technology plus operations plus industry expertise, embedded across multiple functions at the same client over many years — is difficult to replicate at scale. That is the franchise the bulls defend. Where AI fits is precisely the contested ground: it is simultaneously the company’s largest demand catalyst and the largest question mark ever placed over the labor model that turns demand into profit.

Management’s recent moves sharpen the picture of how it intends to defend that franchise. Alongside the third quarter, Accenture announced roughly $4.18 billion in operational-technology cybersecurity acquisitions — a majority stake in Dragos plus all of runZero and NetRise — assets carrying about $208 million of annual recurring revenue growing 48%, an explicit push toward platform-led, recurring software economics rather than pure labor. It also launched Accenture Edge to target mid-market firms with $300 million to $3 billion in revenue, a deliberate move down-market into a client base it historically underserved. Capital allocation remains shareholder-friendly on the surface: fiscal 2025 returned $8.3 billion (including $4.6 billion of buybacks), the dividend rose to $1.63 per quarter, and management committed to return at least $9.5 billion in fiscal 2026. The tension — explored below — is that the same year’s acquisition budget ballooned to roughly $9 billion, funded in part by new debt, even as organic growth slowed.

Sources: Accenture Q3 FY26 earnings release and Form 8-K; FY25 Form 10-K and annual report; company fact sheet; market data at the June 22, 2026 close ($124.83). Figures rounded; valuation metrics on ~614M diluted shares. Net cash has narrowed to roughly $1–2 billion (cash ~$9–10B against ~$8.4B of debt) as the balance sheet levers up to fund acquisitions.

03 — The Bull Case