The Walt Disney Company: Strategic Reset or Structural Decline?

Does D’Amaro’s appointment signal a capital allocation renaissance — or does Disney’s structural decay outrun any single CEO?

Section 1

The Analytical Question

On March 18, 2026, Josh D’Amaro became chief executive officer of The Walt Disney Company, succeeding Bob Iger, who now serves as a senior advisor through the end of the year. D’Amaro is a 28-year Disney veteran, but his entire executive career has been built inside one part of the company: he ran Disney Experiences — the parks, cruises, resorts, and consumer products business that generates the highest returns on invested capital and the most defensible competitive moat in the entire portfolio. Dana Walden was elevated simultaneously to president and chief creative officer, overseeing film, television, and streaming, and reporting directly to D’Amaro. The appointment of a parks operator to the top job — rather than the entertainment co-chair — is not a continuity decision. It is a statement about where the board believes Disney’s value is created. The question is whether the market has priced what that statement implies.

At $104.08 per share, Disney trades at approximately 14 times forward earnings and about 11.5 times forward EBITDA — a discount to the S&P 500 and near the low end of its own historical range. The market is pricing Disney as a structurally challenged media conglomerate whose streaming pivot has consumed a decade of shareholder returns: under Iger’s second tenure, from his November 2022 return to the D’Amaro announcement, the stock returned roughly 7% against a gain of more than 76% for the S&P 500. That is the low bar D’Amaro inherits — and also the source of the opportunity, because a business priced for continued underperformance does not require heroics to reward shareholders. It requires only that the decline thesis be wrong.

This report resolves two questions. First: can D’Amaro’s parks expertise and demonstrated capital discipline genuinely reshape Disney’s financial profile — redirecting capital toward the segment that earns superior returns and away from the value-destroying instincts of the Fox era? Second: are Disney’s structural headwinds — the collapse of linear television, an entrenched streaming competitor in Netflix, and a balance sheet still carrying the weight of a $71.3 billion acquisition — so severe that they are effectively CEO-agnostic, leaving D’Amaro to manage a decline rather than reverse it? The bull and bear cases that follow are arguments about which of these forces dominates.

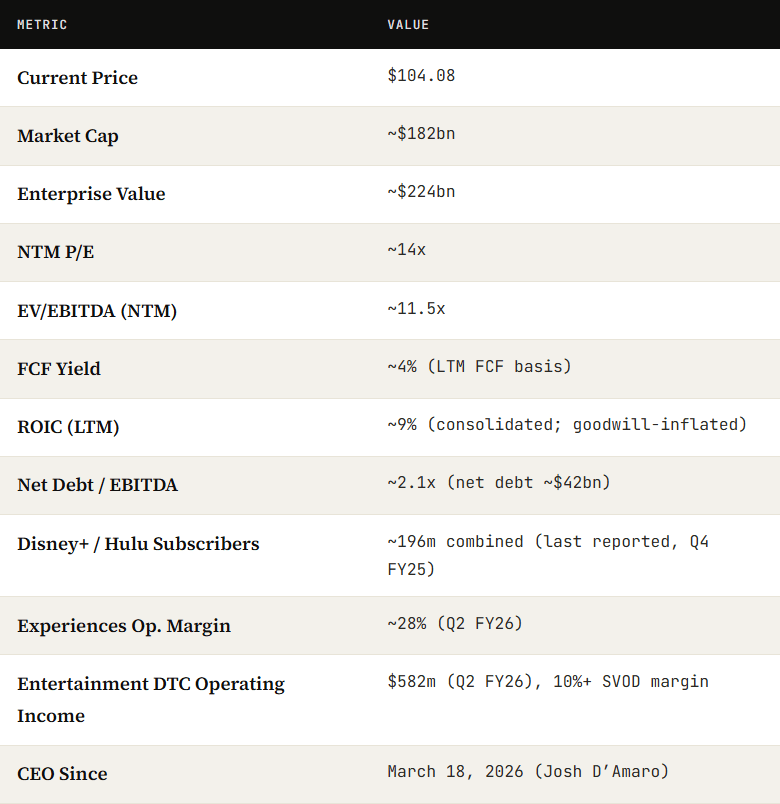

Section 2

Business Snapshot

Disney reports three segments. Entertainment houses the film studios, the Disney+ and Hulu streaming services, and the legacy linear networks including ABC; in fiscal 2025 it generated full-year segment operating income of $4.7 billion. Experiences — the domestic and international theme parks, Disney Cruise Line, and consumer products — produced $36.2 billion of revenue and record segment operating income of $10.0 billion in fiscal 2025, remaining the company’s profit engine: it generated roughly 57% of total segment operating income on under 40% of revenue. Sports, essentially ESPN, contributed $2.9 billion of full-year fiscal 2025 segment operating income, but that income is structurally pressured — it declined 5% year over year in the second quarter of fiscal 2026 as rights costs outran affiliate and advertising revenue. Total segment operating income reached $17.6 billion in fiscal 2025.

The financial trajectory has genuinely improved. Disney’s direct-to-consumer streaming business swung from operating losses of roughly $4 billion in fiscal 2022 to $1.3 billion of operating income in fiscal 2025, and in the second quarter of fiscal 2026 Entertainment streaming operating income rose 88% to $582 million, crossing a double-digit operating margin for the first time. Full fiscal 2025 revenue reached $94.4 billion with net income of $12.4 billion and diluted earnings per share of $6.85, and free cash flow of roughly $10.1 billion. The company has resumed buybacks — targeting at least $8 billion in fiscal 2026 — and reinstated the dividend.

That recovery, however, sits against a capital allocation legacy that must be assessed honestly. The 2019 Fox acquisition cost $71.3 billion, loaded the balance sheet with debt, and forced the suspension of both the dividend and the buyback that historically compounded Disney shareholder value. Iger’s second tenure stabilized the operating business but did not deliver shareholder returns — the stock badly lagged the market. D’Amaro’s appointment signals that the board wants capital pointed at the Experiences business, where Disney is executing a roughly $60 billion, ten-year plan to nearly double parks and cruise capital expenditure. Whether that is a disciplined reinvestment of capital at attractive rates or simply the next large cash commitment is the central question this report tests.

Figures sourced from Disney fiscal 2025 10-K, Q2 FY2026 8-K and 10-Q, and market data as of mid-May 2026. Subscriber figure is the last disclosed total; Disney discontinued quarterly subscriber and ARPU reporting beginning Q1 FY2026.

Section 3